The Market Wasn't As Healthy As It Looked

Over the weekend, news broke that a peaceful agreement had been reached with Iran. By Monday morning, the reaction was immediate. Buyers returned to the market, but what caught my attention wasn't that stocks were higher. Markets move up and down every day. What stood out was where the money was going.

For much of the past year, investor capital seemed increasingly concentrated in a handful of names tied to artificial intelligence. Nvidia, Microsoft, Broadcom, and Palantir became some of the market's favorite destinations. Whether it was earnings, AI infrastructure spending, or enthusiasm surrounding the future of computing, investors repeatedly found reasons to put more money into the same group of companies.

Meanwhile, a very different story was unfolding elsewhere.

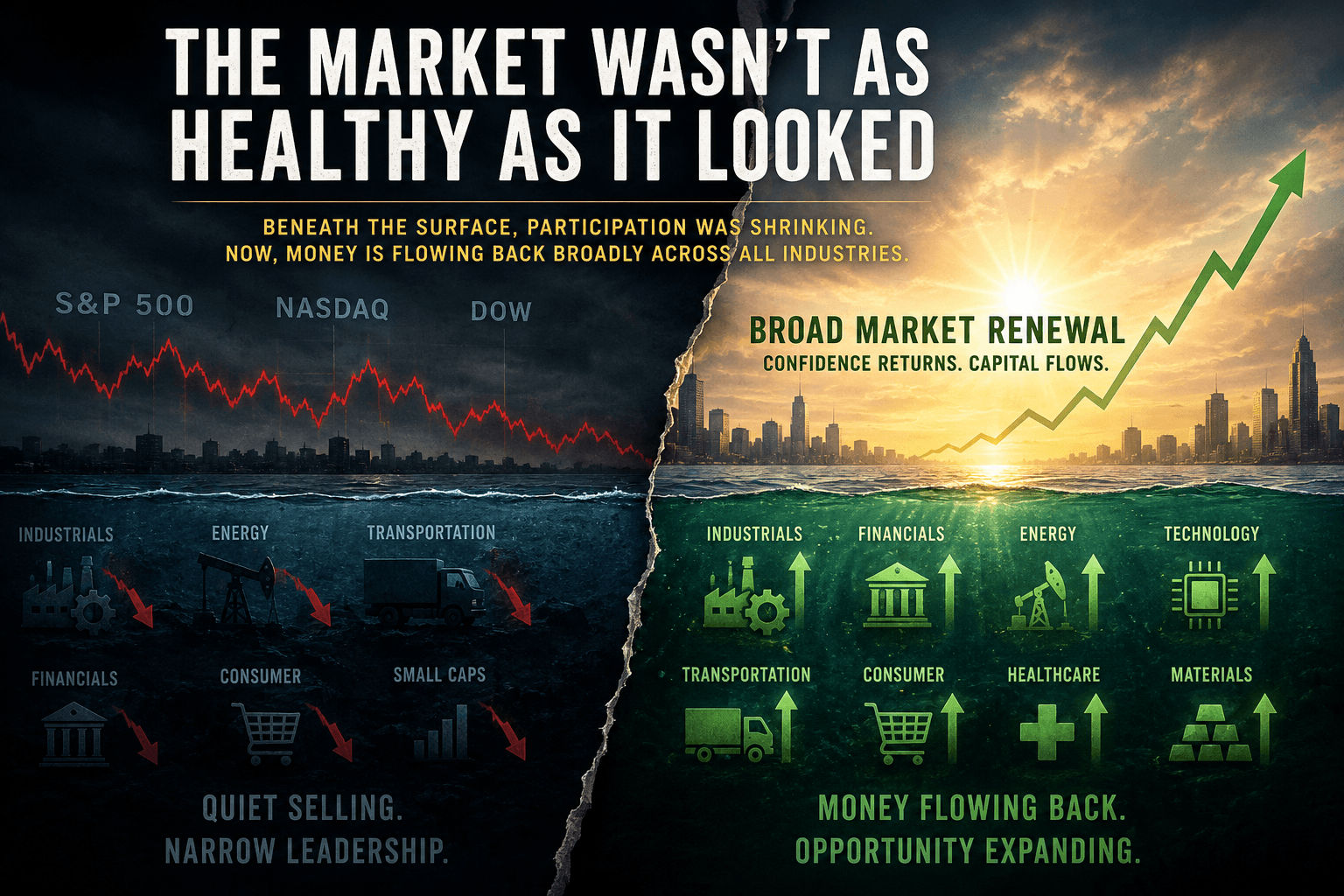

The market looked strong. Large parts of the market did not.

If you watched only the major indexes, the distinction wasn't always obvious. The S&P 500 continued climbing. Technology dominated headlines. Financial television spent countless hours discussing artificial intelligence and the companies benefiting from it.

But beneath the surface, many sectors struggled to participate.

Small-cap companies spent months fighting for investor attention. Transportation stocks often failed to build momentum despite a relatively stable economy. Industrial companies moved sideways. Even areas that traditionally attract capital during periods of economic optimism frequently found themselves ignored. Investors who owned Nvidia or Microsoft were having a very different experience than investors holding regional banks, transportation companies, or commodity producers.

This wasn't a crash.

It wasn't even a panic.

What made the environment unusual was how gradual it felt. Capital didn't appear to leave these areas all at once. Instead, it seemed to drift away over time while more and more money concentrated around a small number of themes. Artificial intelligence became the dominant story, and much of the market began trading as though that was the only story worth telling.

The averages continued climbing while participation quietly narrowed.

That's why Monday felt different.

The opening bell brought buyers into areas of the market that had spent months on the sidelines. Financials attracted attention. Industrials moved higher. Transportation names found buyers. Energy stocks reacted positively. Instead of capital flowing into a single theme, it appeared willing to explore multiple sectors simultaneously.

That shift matters because healthy markets are rarely built on one idea alone.

Nvidia can lead a market.

Microsoft can lead a market.

Artificial intelligence can certainly lead a market.

But durable bull markets are usually characterized by participation. They occur when investors are willing to take risk across a broad range of industries rather than concentrating capital into a handful of perceived winners.

For months, that broad participation often felt absent.

Monday was one of the first sessions in a long time where it appeared to return.

That doesn't mean every problem has been solved. Markets have a habit of changing direction without warning, and one strong day doesn't automatically create a new trend. The coming weeks will reveal whether investors truly believe geopolitical risks have declined or whether this was simply a temporary relief rally.

Still, market behavior often reveals what investors are thinking before they ever say it.

The response to the Iran agreement suggested something important. Investors weren't simply buying technology. They weren't simply buying artificial intelligence. They were buying a wider range of businesses, sectors, and opportunities than they had been just days earlier.

For the first time in a while, the market didn't just look strong. It felt strong.

Perhaps that's the real story.

Not the agreement itself.

Not the headlines.

But what happened when investors suddenly felt comfortable looking beyond the handful of companies that have carried the market for so long.

Because sometimes the most important thing in a market isn't how high the index climbs.

It's how many people are climbing with it.

-

About the Author

Scott Tilley is the founder of TilleyWorks, an independent operational media company exploring media, markets, technology, and systems. Through Intelligence Briefings and Media Broadcasts, he shares observations, analysis, and perspectives designed to help readers better understand a rapidly changing world.

The views expressed in this article are for informational and educational purposes only and should not be considered financial advice.